There’s a saying that goes: “Make new friends, but keep the old. One is silver, the other gold.”

At Optimist, we took that saying to heart and baked it into our entire growth and business strategy.

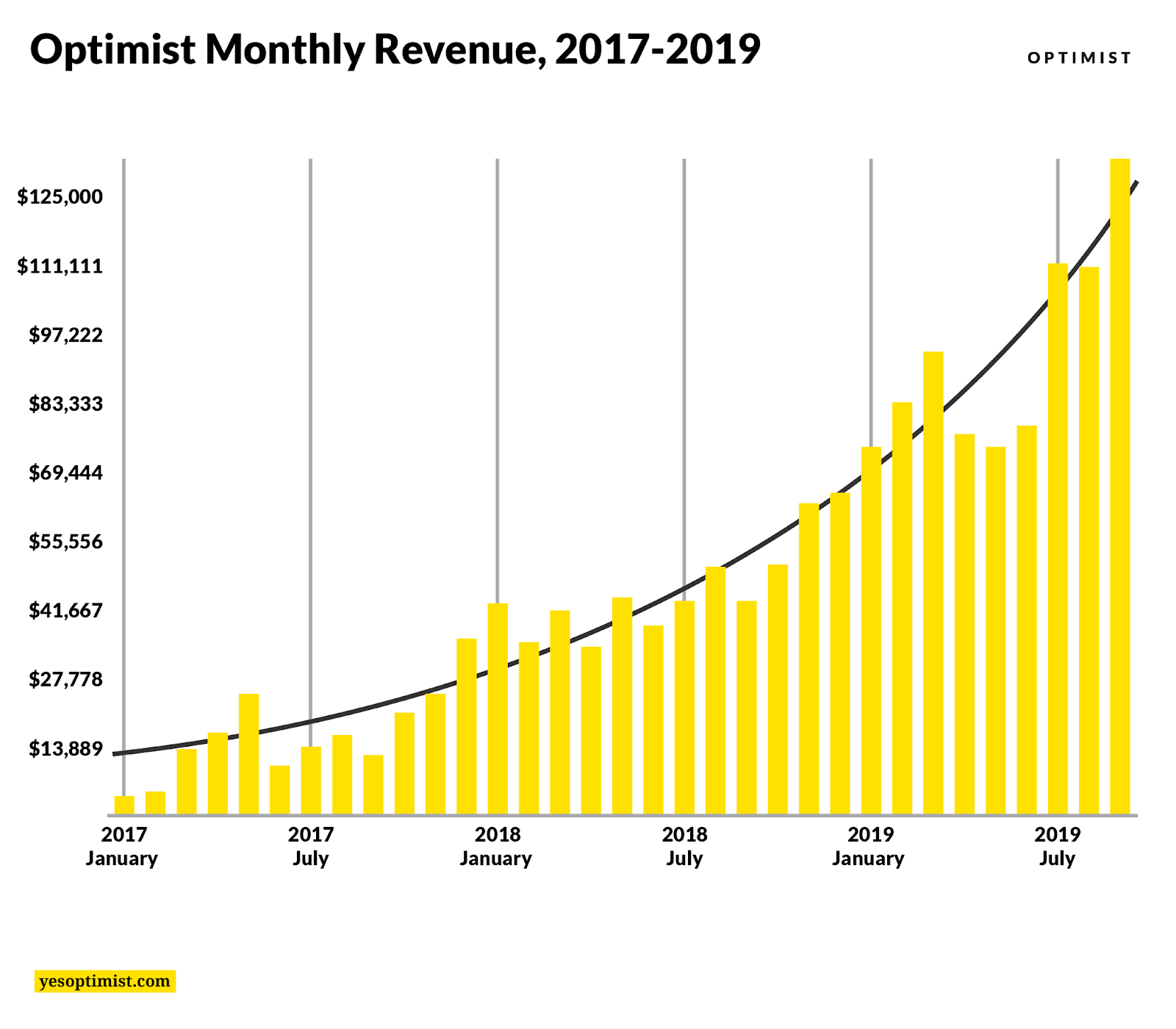

In our first 36 months as a content marketing agency, we grew from $0 to $1.5 million in ARR while working with fewer than 30 companies. At the moment, we have 16 clients, and the average tenure of each client is more than 20 months.

As an agency, we grew primarily through relationships and retention versus new customer acquisition.

We still venture out and put effort into landing new clients, but we place more value on building long-term, strong relationships. Prioritizing our existing clients has allowed us to generate stable revenue and solid ground to stand on — and to grow.

In this post, I want to share what Optimist has done differently to drive growth through retention — and how other agencies and service businesses can do the same.

%(tableofcontents)

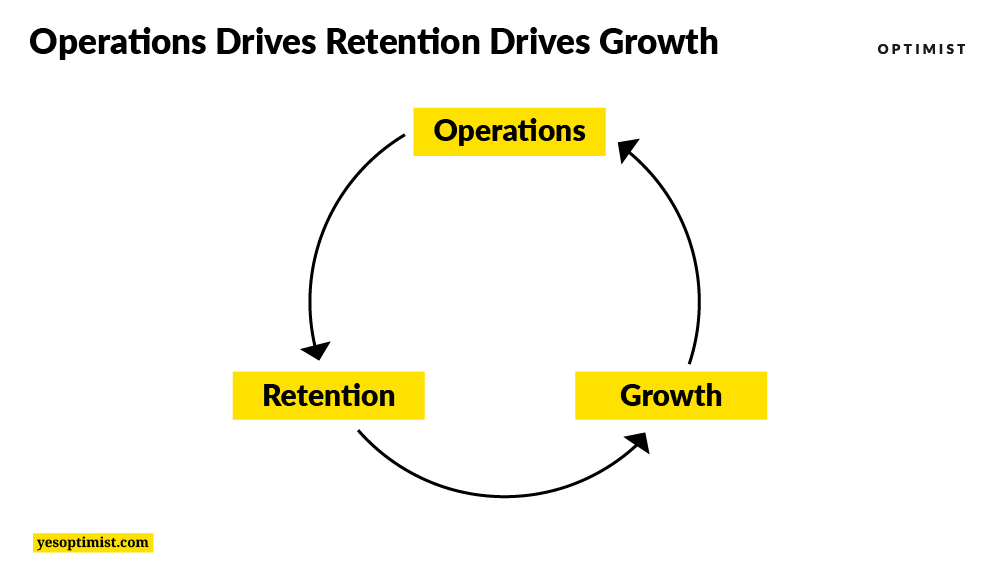

Retention Is Driven By Operations — Getting Things Right

We realized early on that we don’t want to be an agency that’s constantly churning through clients, forced to knock on doors and make cold calls just to keep the lights on.

That naturally led to relying on content marketing and SEO to drive inbound leads. We liked the inbound model in the first place because we wouldn’t need to pound the pavement just to find new clients.

But, we felt the best way to make the inbound model work was to focus on not only the acquisition parts of the strategy, but the retention parts as well.

If we had to go out each month and find new clients to replace the ones that stopped working with us, it would put a lot of pressure on our marketing to keep the pipeline full.

However, if most of our clients keep working with us long-term, each new client would mean new net revenue — rather than merely keeping us treading water.

And, for us, this has really worked.

The main driver of our success in retaining customers is our operations.

Operations is the nuts and bolts of our business that keeps us running smoothly. If your workflow doesn’t scale to accommodate a growing volume of work, the quality suffers, and so do your clients.

This process is something to work on and improve continuously as your business grows. Where possible, strive to minimize busywork and reduce repetitive tasks.

By streamlining operations, you can ease the burden of administrative tasks, freeing up more of your team’s time to be creative and productive. Now, let’s see how we do just that.

1. Documenting New Client Processes And Onboarding

Documenting and automating as much work as possible when onboarding new clients is crucial to our operational success.

Onboarding sets the tone at the beginning of a new client relationship. This is when the client feels most vulnerable — they’ve just laid out a big expenditure, after all — and are holding their breath to find out if they’ve made the right choice.

From our agency's perspective, onboarding represents a key opportunity. It's our first opportunity to prove to the client they’ve made the right choice.

It’s our chance to demonstrate our commitment and set the cadence for the entire relationship. If we deliver — nay, overdeliver — during this precious onboarding window, the client will see us as a reliable partner they can count on to go above and beyond.

That’s what good client relationships are made of.

So, how do you go about documenting your onboarding process?

The first step is to audit your current strategy.

We’ve iterated on our onboarding process over the years by annually reviewing each of our engagements. During retreats or team-wide Ops Jams, we methodically assess our current process and its effectiveness.

In this process, we look back at the clients we have brought on over the previous period:

- Are they still working with us? What is the Lifetime Value (LTV) and engagement length?

- How strong is the relationship? This is a subjective measure of how connected we feel to their team and company.

- What steps were involved in the onboarding process?

Each client is scored on how well we think we found a stride in the onboarding and what the onboarding process looked like in retrospect.

We also review each of the onboarding tasks and processes. We ask the team to identify holes in that process, places where they had questions, or oversights when information wasn't clearly communicated.

Based on this process, we have refined our onboarding workflow over the years. We’ve expanded the steps involved with bringing on a new client. One of the most notable changes was adding two separate “kick-off” calls:

- Internal kick-off with members of our team who will be working with the client.

- Full-team kick-off call with our team and the client.

This first call gives us space to set expectations and collect questions internally before we sync with the client. It also creates some “safe space” for the team to ask questions or get clarification without having to do it in front of the client.

2. Scaling The Team Effectively

Operations are driven by people. Without people — the right people in the right roles — things just won’t get done.

As with onboarding new clients, you also need to think about growing and onboarding new people for your team as well.

A critical, overlooked, and pain-inducing part of growing a business is not having the right people when you need them. Lack of talent can literally stop your growth dead in its tracks.

This means you need to be proactive, tracking your team’s workload and capacity, generating new applications, and planning your hiring needs before it’s too late.

It's funny. Most agencies don’t think about how they scale their team or their hiring and onboarding practices until everything is already on fire and they’re desperate for a solution.

Don’t make that mistake.

HR tasks are some of the most repeatable systems in every industry. You’ll need them from day one, and your needs will only continue to grow.

For us, this meant scheduling, automating, and streamlining our entire process for bringing on new team members.

I think it’s important to invest in automating time-consuming processes by using software. This will streamline your workflow and allow your team to focus their energy on tasks that fully utilize their knowledge and skills. Set up a system that works for your business’ hiring needs, from selecting new employees to onboarding them.

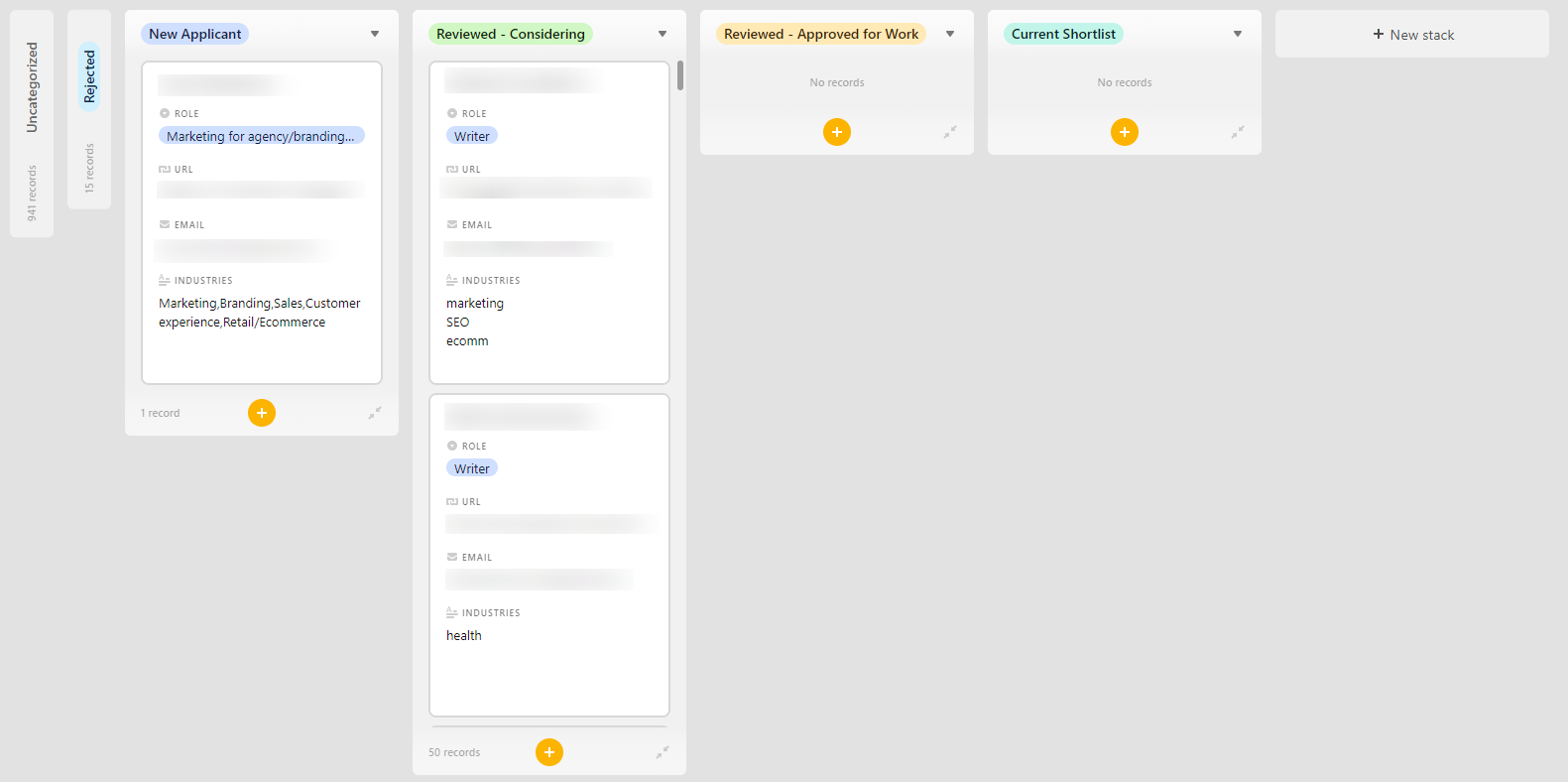

Here’s a snapshot of the Optimist recruiting process:

-

Call for applicants. We cast a wide net with job postings on several platforms. To date, our most successful listings have been on Reddit and Angel.co. These seem well-suited for us because their user base is a more sophisticated internet user, often familiar with startups and our core work.

-

File applicants. Each person who applies completes a Paperform submission. Zapier sends these submissions to an Airtable, including the details in a Kanban-style board where we can review them individually.

-

Filter vigorously. About 90% of applicants are disqualified. Most commonly, we disqualify applicants based on work experience (or lack thereof). At this stage, we want to know if the applicant’s previous work seems to align with the kind of work that we do at Optimist. That means a history of creating strategic, in-depth content, ideally for technology and SaaS companies or startups.

-

Pilot project. Once we have decided to work with an applicant, we do a paid pilot project using a current client project. The prospect will work with existing team members who have experience working with that client to provide feedback and finalize the work.

-

Team onboarding. If the pilot project goes well and the prospect seems to be a fit, we begin onboarding them to the team, helping them understand our culture, and bringing them up to speed on our processes.

We use Notion as a central repository for onboarding, as a Wiki, and as a way to store and manage incumbent knowledge.

3. Streamlining Finance To Make Sure Everyone Gets Paid

Now that we’ve discussed how to onboard your customers and scale your team effectively, it’s time to streamline finances and bookkeeping.

As Optimist has grown, a time-consuming task has been managing our finances.

Your business will start with a small amount of financial work: one or two client invoices, a few people on your payroll. But as you grow, the paperwork gets harder to manage. Imagine having to write hundreds of checks and invoices by hand. Mistakes are bound to happen, not to mention the slow speed of this system.

With each new client, each new team member, and each new retainer, the effort and complexity of keeping your books can scale exponentially.

More importantly, the accuracy and precision of your accounting matters a lot.

As a service business, our entire model is dependent on our ability to manage cash flow. If we can't accurately track what we spend and forecast our future expenses, we could easily find ourselves with a healthy business but a negative bank balance.

These two factors — complexity and precision — are what make accounting such an important business function to outsource to software (or experts, but software is a lot cheaper!).

I found that using software is an important ingredient for managing the financial health of the firm. Not only has this saved me countless hours, but accurately tracking and managing expenses (including payroll and invoicing) has been easy to automate even as our business scales.

Automating the financial stuff can feel like a no brainer, but for many business owners (myself included), it can be difficult to let go of the details.

It was challenging for me because intimately knowing the financials gave me confidence that things were under control. I had my hand on the wheel at 10 and 2; nothing could slip by.

Relying on automation adds a layer of obfuscation that can be scary.

I’ve taken a phased approach that allows me to prove to myself that I didn’t need to keep a tight grip on every penny and manually enter every expense for things to work.

I have outsourced and automated several financial tasks as we’ve grown:

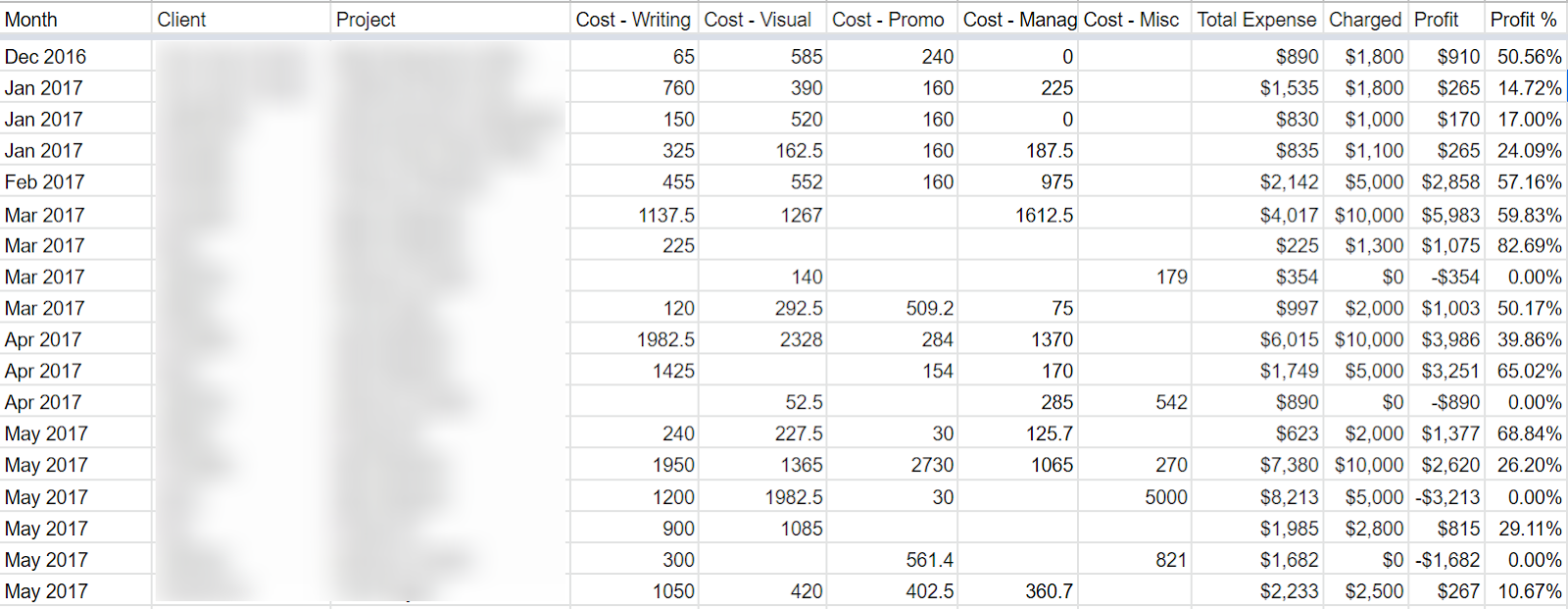

P&L/Client Tracking

In the early months of Optimist, as we grew from $0 to our first $10k-20k MRR, I knew that I wanted and needed a more granular financial report than what I could get out of the box from my accounting software.

Namely, I wanted to track categories of expenses and segment them by client.

This was critical because it allowed me to track and analyze our profitability for each client and track expenses for different functions across the team. If we spilled over our margins, we could identify where those overages occurred and take steps to fix it the next month.

To do this, I built a simple automated spreadsheet that tracks and parses our cash flow based on function and client. It's still the main financial report I track today.

Expense Tracking

One of the most tedious tasks is tracking all the tiny expenses — from meals and travel to software licenses, tax payments, and internet service.

Luckily, this is easy to automate.

I create recurring expenses in Freshbooks and sync my bank account to have each of these little bits generate an expense automatically, then I categorize and reconcile those costs.

After we grew to around $50k MRR, it was clear this convenience was critical to juggling the books without spending a bunch of time trying to make sure they were always pristine.

Audit/Reconciliation

As we have grown to $100k+ in MRR, our financials have become increasingly more complex.

We are in an awkward stage where we have enough transactions posting each day or week that it takes up a lot of time, but we are nowhere near big enough to need a full-time person to keep the books.

So, we have implemented a partial solution.

This piece has not been fully automated, but I have been able to outsource it.

Rather than painstakingly poring over my financials every week or month, I simply have a VA who helps by performing an audit and reconciliation on our financials every few months.

They cross-reference all our transactions, categorize and detail any unmarked expenses, make sure that the expenses match the bank statements, and add in any expenses that may have been missed.

This saves me tons of stress, and it only takes them a few hours per quarter.

Invoice Processing

Now that we are hovering between $100k-125k MRR, my next goal is to automate invoice processing.

I receive and process between 5 and 20 invoices each week. This isn’t an unmanageable number, but it is a process that sucks 1-2 hours of my time every week. It often has to be pushed back in my day, which can delay payments for our team.

My goal is to build a unified invoice inbox that will take this process and turn it into a 10- or 20-minute task where expenses are quickly approved and then automatically tracked, processed, and paid using accounting and invoicing software.

By taking a phased approach, I’ve been able to loosen my grip without feeling out of control. I’ve freed up time, energy, and mental space to focus on the other elements of the business that matter most.

4. Delegating And Distributing Work

Leadership is most effective when the leader knows how and when to delegate.

Now, with riskier elements like recruitment, distributing work can be challenging. Should you trust someone else with this?

The answer is a resounding yes — but only if you do it the right way.

One study has shown that CEOs who delegate work generate 33% more revenue than those who don’t.

In the example of delegating recruitment, you could delegate preliminary research and outreach to relevant team members, but still retain control over final decisions.

Approving job descriptions, selecting top candidates, making offers, and designing onboarding processes should come from you. However, finding candidates, creating job descriptions, and interviewing candidates should be delegated.

Unfortunately, I haven’t sat down to quantify each activity and how productive it is.

One framework that I use is the idea of $10, $100, $1,000, $10,000/hour work.

Here’s the fundamental question you need to ask yourself as an entrepreneur: What time and activities are you doing that create the most value for you and the rest of your team?

And, inversely, which activities are blocking you from doing that work?

For me, it’s sales and marketing activity for Optimist itself that generates the most value.

If I can spend 15 hours per week helping us get one new client that ends up being worth $150,000 in revenue, then I’ve just done 15 hours of $10,000/hour work.

If I get bogged down focusing on the day-to-day work, even if it’s highly valuable (say $100/hour), that is eating up time that I could be spending on activities that generate 100x the value.

So, whenever I add items to my task list, I try to ask myself which bucket that work falls into.

I can’t eliminate every administrative task, of course. But I can strive to make sure I am spending the majority of my time on the highest-value work — and try to delegate the rest.

One of the keys to doing that is giving the rest of the team the skills and knowledge they need to execute at a higher level. That means I can trust them with more of the tasks that are eating up my time.

5. Invest In Training And Education

When we first started Optimist, I was the point person for almost all the work we did with clients. I was the contact, the strategy director, the account manager, and — in many cases — the writer!

I did it all.

Not only was this unsustainable (both for me personally and for the business as it scaled), but it was freakin’ dangerous.

This is a single point of failure. If I got sick and couldn’t work, the entire team would be in trouble, not to mention the clients. There was no plan B.

That’s why a key step to keeping your clients is training and leveling-up team members across the board.

You want your business to run like a well-oiled machine with no single point of failure. And the major components of that machine are your employees. If one fails, and the others can’t do their job properly, the dominoes start to fall, and you risk impacting your clients.

You can safeguard against failure by investing in your team’s education — everything from your company’s processes to industry standards and other aspects relevant to their positions. When your employees know they are valued and have opportunities to advance their skills and knowledge, they’re more motivated to keep your clients satisfied. A study found that companies whose employees are engaged outperform companies whose employees are not engaged by up to 202%.

The way that I quantify this kind of investment is in relative terms.

Earlier I mentioned how my goal is to spend as much time as possible focused on doing $10,000/hour work.

For me to focus my effort there, I need my team to do $100/hour work and $1,000/hour work. If they can complete this high-value work, it frees up more of my time to focus on the top tier.

Even better, if the team can do $10,000/hour work, then we achieve a real force-multiplier.

For the team to work at this level, we need to invest in their training and education. For us, this means creating space and time to learn and grow. We have three key mechanisms for this:

- Ops Jams. Monthly time dedicated to discussing and solving any operational challenges

- Retreats. Twice-yearly in-person meetups where we collaborate on new ideas and solve problems

- Ongoing training. Ad hoc feedback, training, and learning opportunities

In total, we invest ~$100,000 per year in this training.

The math on this is simple.

If investing $100,000 in education means that I can spend an hour a week focused on $10,000/hour work rather than $1,000/hour work, then I’ve just netted about $300,000 profit.

Better yet, if each person on our team (20 in total) could do one hour of $10,000/hour work each week, then we’re talking about millions of dollars in return.

Invest in your team. It’s worth it.

Getting Everything Else Right, Too

My philosophy has always been that getting the internal parts right is the foundation for everything that you do externally. But that doesn’t mean it’s the whole picture.

The entire point of delegating and elevating the team isn’t so I can lay out on a beach somewhere with all my free time. It’s so I can spend more time thinking and acting strategically where it matters most.

One of those key areas is the client relationship.

The truth is that most companies want to improve retention. But they aren’t sure how to accomplish that goal in an actionable way.

Should you change up your prices or diversify your services? Send thank-you notes? Offer a loyalty discount?

There’s no one-size-fits-all solution for improving client retention. Instead, what we’ve learned is that there are small and actionable points of leverage that you can bake into your processes to create stronger relationships.

At the end of the day, many relationships hinge on small moments and tiny actions that tip the scales in your favor. Building a track record of delivering above and beyond the client’s expectations can protect your reputation and relationships in the face of unexpected challenges.

These scenarios are inevitable. The best course for agencies is to focus on building strong client relationships that can withstand trying times.

To retain a client, you need to understand the specifics of what makes a good partnership.

6. Creating A Shared Identity Through Brand Values

One thing I’m most proud of is how committed our team is to Optimist’s brand values. We start most discussions with our prospects with these ideals about the kind of work we want to accomplish and the type of relationships we want to forge.

This may seem corny or overhyped.

“Everyone has 'brand values' and usually they mean nothing.”

But we take them seriously. We think a lot about how these values are propagated through everything that we do as a firm. Most importantly, I craft our vetting, onboarding, and workflow processes to reflect those values and prove that they aren’t just marketing crap. They actually matter to us — and they matter to our clients, too.

When I jump on a call with a prospective client, I can tell right away if they’re going to be a good long-term fit for us. In almost every case, they mention that seeing our values on the website played a large role in their decision to choose us over other content marketing agencies.

From my perspective, this means the foundation of every client relationship is built on more than dollars and cents.

We have a shared identity with our clients. We are aligned on a moral and philosophical level that can transcend the logistics of a purchase or business transaction. That’s extremely powerful and, I think, a huge part of the competitive advantage that drives our client retention.

7. Aligning Your Goals And Interests

One of the most fundamental pieces of a vendor-client relationship is aligning incentives.

Unfortunately, many agencies are simply structured to extract money from clients, regardless of whether that extra spend actually benefits the client or translates into meaningful ROI. We see this constantly in the form of unnecessary upsells, inefficient spend, and subpar work quality.

When an agency’s incentive is to maximize profits, the focus is increasing revenue and decreasing costs.

Meanwhile, the client’s incentive is to minimize their agency costs and/or generate the best outcome from the relationship. Or, more importantly, to generate a positive return on the investment in these services. (Most smart clients are less concerned with absolute budget and more concerned with ROI.)

These incentives are not aligned — they’re opposed.

This is a toxic scenario.

The second your clients begin to question whether you have their best interests in mind, the relationship is in decay. That seed of doubt will blossom into a full-blown sense that maybe you aren’t serving them, but are really focused on serving yourself.

What clients really want and need is a partner that will unequivocally work in their best interests, even if that sometimes comes at a cost to the firm.

Now, Optimist isn’t exactly bending over backward to give away free work or dip into our profits. (We’re still a business after all). But we do a lot of things differently to make sure that we have skin in the game:

-

Month-to-month contracts. No one is locked into working with us. If we aren’t delivering, we get cut.

-

Weekly scorecards with detailed reporting. We review our performance every week to understand the work that we’re doing.

-

Defined business and growth goals. Each engagement starts with a specific goal in mind. We track metrics toward these goals in order to help achieve the specific outcome.

If we look at our weekly scorecard, it’s a simple report.

But each client has their own reporting. Based on their specific goals, we track progress toward that high-level outcome and KPIs that work as leading indicators. We want to capture a 360-view of the work that we’re doing and how it’s improving business performance.

All in all, I tell clients that we can never guarantee a specific outcome. But we can make sure that our incentives — to keep the client paying us each month — are aligned with their business goals of achieving growth.

We monitor and assess this progress together, making sure that the client is happy with the outcome from their investment.

8. Engineering Intentional Reliability

We all know that clients expect their vendors to be reliable.

But how do they decide if you are, in fact, a reliable partner?

Science says it’s not as straightforward as showing up. It’s about finding points of leverage — showing up when it counts most — and being intentional about how you cultivate the expectation of reliability.

The Pygmalion Effect describes how our actions shape others’ beliefs about us, which perpetuates a cycle that reinforces those beliefs. This is a powerful force, and the momentum is important.

In other words, it’s about being intentional and strategic in shaping that perception.

As in every relationship, there might be times when you can’t deliver exactly what the client wants. Maybe communication lines get crossed, expectations get misaligned, or someone gets sick and misses a deadline. Whatever the case, it’s important to acknowledge that these things can happen; depending on the client’s perception of you, it can impact the relationship.

You need to be intentional about setting an expectation of reliability. Make sure that if something goes wrong or there’s a hiccup in the relationship that it's the exception rather than the rule.

Remember, the key here is to be both reliable and intentional.

-

Be reliable. Reliability is essential to having a good relationship with your client. You need to be there when they need you; they need to be able to count on you.

-

Be intentional. Doing things without understanding them doesn’t cut it. You need to understand what brings value to your customers and then do it.

Hard Work Earns Customers

We’ve talked about the value of retaining long-term clients, building scalable internal operations, and focusing on retention to drive growth. These elements are so closely interlaced that you can’t afford to ignore a single one.

The key to retention lies in refining your operations. Unlocking retention, inevitably, brings growth.

Many churn-and-burn shops storm into the marketing world, gobble up hundreds of clients, look sexy on paper, but ultimately create a toxic environment for their team and for their clients. These shops aren’t usually built to last.

I’m focused on building a foundation of growth that can scale without cutting corners. That means investing in retention and putting in the work to perfect operations.

In the words of Christopher "Big Black" Boykin (RIP), “DO WORK!”

Tyler Hakes is the Principal and Strategy Director at Optimist. He's spent nearly 10 years helping startups, agencies, and corporate clients achieve growth through strategic content marketing and SEO.

Add A Comment

VIEW THE COMMENTS